2023 Year End Recap

2023 Year End Recap

January 18, 2024 by Lesjak Planning

“How is it that our investment portfolios report a gain in a year that was supposed to be such an utter disaster?”

This is the question we hear daily as clients receive their annual reports. The talking heads and financial “experts” all predicted market chaos like never before as inflation scares would cause the Federal Reserve to raise interest rates to a point of driving our economy into recession.

As the Fed rates rose from near zero to 5.5% in a matter of months, stocks and bonds declined as investors fled to the safety and yield of short-term investments. All were preparing for the coming touted recession. Except it never came.

Our nation and world economies ebb and flow constantly with periods of prosperity and recessions occurring all the time. As witnessed multiple times in our past, the lesson here is not to rely on the predictions and advice of media stars when making decisions regarding your personal financial circumstances. Simply, no one knows exactly how the future will unfold.

2023 again brought us a year marked with geopolitical uncertainty caused by wars, shipping disruptions, continued terror threats and international protests. On the home front we experienced inflation, job cuts, rising homelessness and immigration issues. Political and judicial decisions caused further divisiveness among our citizens. One might assume that consumers would hunker down and restrict spending in the face of all the negativity. That did not happen.

The U.S. generates about 70% of its GDP from consumer spending. After Covid, consumers spent vigorously using the government stimulus money received from the pandemic. Those that did not spend, either saved the payments or paid down outstanding loans. As we moved through 2023, it was expected for consumers to reduce spending as those government checks ran out. In reality, spending continued as shoppers simply used those extra savings built up or reverted to the use of credit cards. The savings rate in the country again dropped below 5% and credit card debt has ballooned to all time highs over $1 trillion. The reason we have not experienced the assumed recession is the fact that Americans never stopped spending! At some point, the record amount of consumer, corporate, and government debt will need to be addressed. But that keeps getting kicked down the road.

Equity markets were in a range for most of 2023 experiencing gains into July, then giving back most into October. As data then began coming in showing economic growth slowing a bit along with inflation numbers, the Fed began to change their strategy from continued tightening of the money supply to a possible pause in rate increases. At their December meeting they went so far as to suggest making multiple rate cuts beginning in March. Since stocks and bonds normally do well in periods of falling rates, this sent a rush from cash into the stock and bond market. Since October, the S&P 500 index rose 11.6% until year end. Broad based trading occurred across most sectors as the fear of missing out took over. For the year, The S&P 500 index gained 26%, Nasdaq gained 44%, and the Russell small cap index gained 17%. After a historical decline in 2022, bonds also rebounded strongly on the Fed change in strategy.

Regarding the various investment sectors, there are numerous positives in the data. Advancing stocks verses declining stocks are currently at a multi-year high. 60% of the S&P 500 company stocks are above their 200-day moving average which is good. About $5 trillion still remains in short-term savings instruments. Yields have also risen on bonds to numbers we haven’t seen in decades and if interest rates do decline, bond prices will increase. Presidential election years have historically seen the S&P 500 gain on average 6%. So, although there has been good growth in the markets recently, we could see continued increases in values.

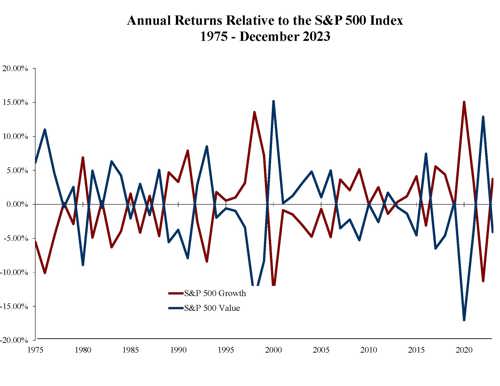

Historical graphs can show the difference in performance over the years between the Growth style of investing and the Value style. The Growth style mostly consists of smaller and mid-sized companies whose objective is to get bigger by investing profits back into the business. In the Value style, we find larger more established blue-chip type companies that tend to hold their value while also returning profits to shareholders in the form of dividends. Comparison of the two over various time periods can provide substantial performance differences. Over longer-term periods though, one or the other reverts back to their mean after a period of outperformance and produce very similar returns. With the future being an unknown, we believe it is prudent to balance investments designated for equities between the sectors according to your individual needs. This strategy has performed very well over time.

Happy New Year!

The Lesjak Planning Team - Dave, Mike, Marc, Nathan, Kevin, Kathy, Ryan

Farewell to 2023

We close the books on 2023 acknowledging that it was surprising to many. We have been in this business longer than most and realize that markets go their own way and perform to no one’s expectations. We turn our attention to the present and also acknowledge that most of the uncertainty in 2023 continues this year with more likely to come. Alas, we face another election year and the media circus that always accompanies the process. We currently are a divided nation on many fronts and the issues that divide will no doubt be front and center as we approach November. We all have the privilege of a vote in the outcome. Hopefully most will use it.

About the author

Lesjak Planning